Pattern Recognition in Turnarounds

Deutsche Bank(2021), Citi(2022) and Fiserv(2026)

Disclaimer: Not financial advice. DYODD. I currently hold long positions in several companies mentioned in the article.

I’ve Seen This Before

2021-22’s Deutsche Bank. 2022-23’s Citigroup.

Both were deeply out of favor. Both sought new leadership, successfully turned around, and rewarded patient shareholders with gains of 3 to 4 times from their trough in 3 to 4 years.

They share a pattern: a strong franchise temporarily impaired by operational mismanagement, with a new CEO who took time to analyze the problems before acting, and then implemented realistic plans.

Last month, I published a Fiserv deep dive suggesting a similar setup is forming. If you haven’t read it, start here; today’s piece builds on it.

This is the follow-up. The May 14th Investor Day 2026 was a new data point: testing whether Mike Lyons (new CEO) truly understands the depth of the problem, and has what it takes to fix it.

The Turnaround Pattern

The table below tells the story. Successful turnaround leaders share one trait that failed ones don’t: patience. They spend 12–18 months understanding the problem before committing to a plan. They set realistic goals and resist the urge to announce grand visions early.

Deutsche’s Sewing waited 15 months before laying out the “Compete to Win” strategy: exiting the money-losing equities desk and returning Deutsche Bank to its roots. Citi’s Fraser waited 12 months before her investor day: exited retail banking across 14 countries and refocused on institutional strengths. In both cases, the turnaround took a while, and patient investors were rewarded.

The failures moved fast. Marissa Mayer at Yahoo and Ron Johnson at JCPenney both charged in with sweeping changes within weeks, and both failed spectacularly. Real turnarounds aren’t about speed or grand vision. They’re about deep understanding and measured execution.

Let me be clear: I’m not saying that waiting 12 months before launching a plan is the holy grail of turnarounds. But there is a clear pattern and strong logic for what makes turnaround CEOs successful.

That’s the setup for today’s discussion on Fiserv’s Investor Day 2026, 12 months after Lyons became CEO in May 2025.

Fiserv Investor Day 2026

When evaluating a new management team, I care less about headline targets than thought process: how they identify problems, diagnose root causes, and set measurable goals. That discipline is what separates turnarounds that deliver from ones that disappoint.

With that lens, here is how it handled two critical issues during Investor Day: Core banking attrition and Clover growth.

#1 - Core Banking Attrition

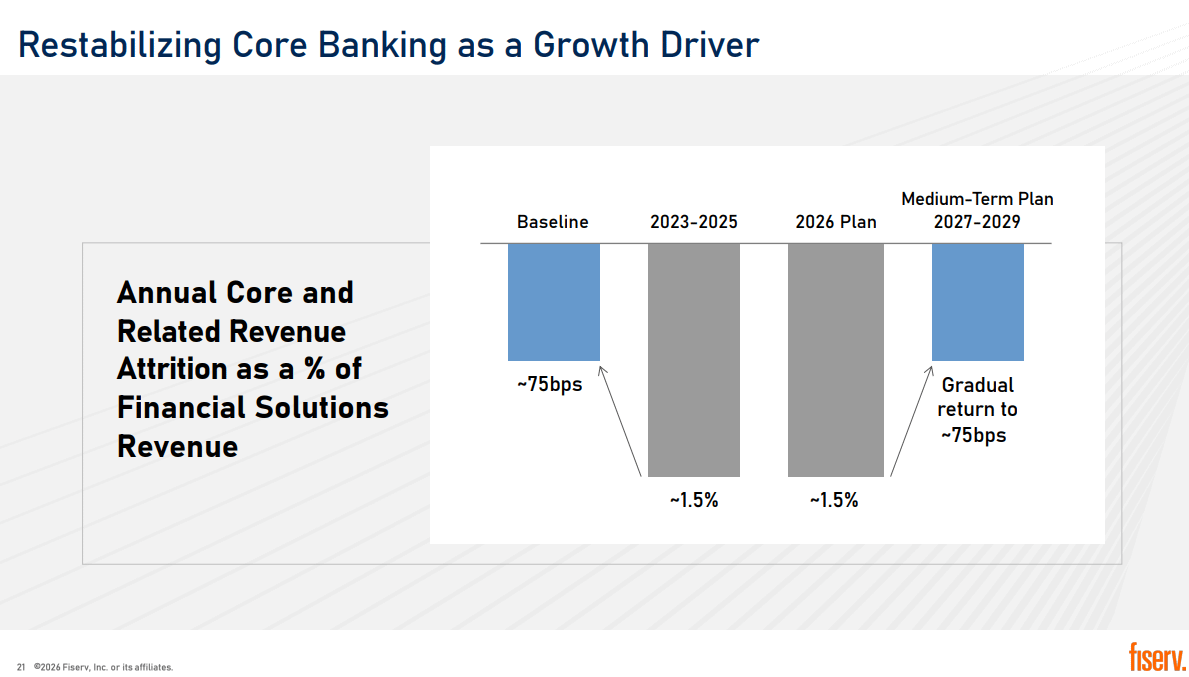

The Problem: Core banking revenue attrition has doubled from its historical ~75 bps norm to ~150 bps since 2023. Its 2.7x revenue multiplier effect ($1 core drives $2.70 in total revenue) amplifies it by 4x.

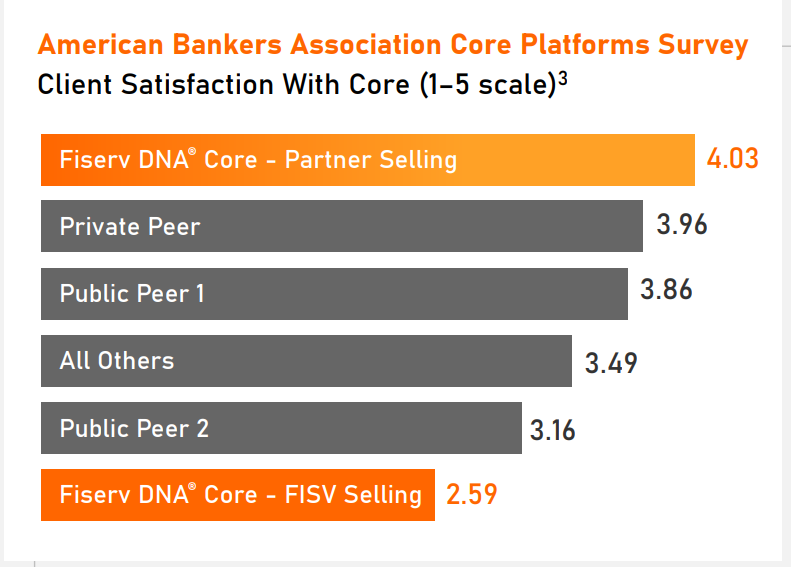

The diagnosis: “Service issue, not technology issue”. The ABA survey validated it: Fiserv's DNA core finished both first and last simultaneously — 4.03 via partner channel, 2.59 via Fiserv direct. Same product, different experience.

The plan:

Reverse forced conversions. The 2022 plan to consolidate 16 cores into 5 on a non-consensual timeline was the primary driver of attrition. Lyons abandoned it to stop the bleed: clients modernize how/when they want.

Rebuild the direct channel. More client-facing headcount, better coverage ratios, cleaner escalation paths.

Acquire Smith Consulting Group. Brings partner-quality DNA expertise in-house, addressing both the expertise and headcount gap in the direct channel

The Goal: Return attrition to ~75bps by 2027–2029, with 2026 held flat as the transition year. It might disappoint some at first glance, but three structural lags explain the timeline:

Multi-year contracts mean departures already noticed can't be reversed;

Service credibility takes quarters to rebuild.

New wins (record 2025 sales, 2026 tracking ahead) take 12–18 months to appear in revenue.

#2 Clover Growth

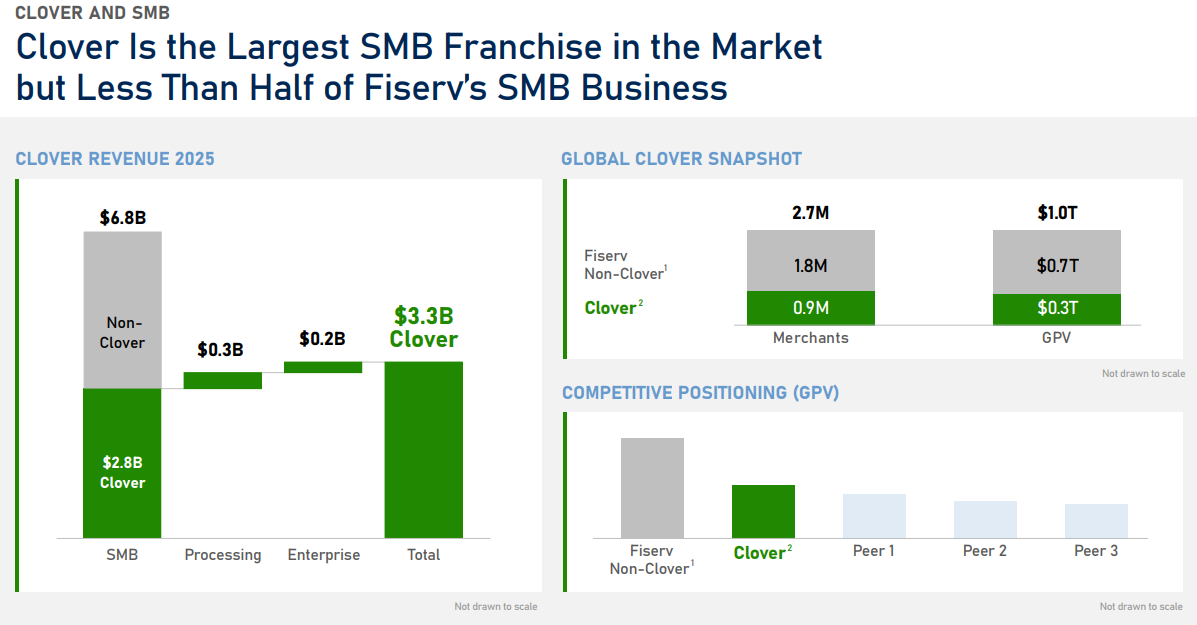

The Problem: Clover's GPV growth has decelerated to ~10%. The market narrative is "fintechs eating Clover's lunch." ~1.8M non-Clover SMB merchants remain on legacy Fiserv undermonetized.

The Diagnosis: while the competitive threat is overstated, as Clover’s ~10% GPV growth matches the broader market, its under-monetization problem persists (i.e., low VAS penetration across the base and non-Clover SMB merchants staying outside of Clover).

The Plan

Convert non-Clover merchants. 1.8M captive SMBs on legacy are a ready upgrade pool. Hardware-agnostic Clover (1H 2027) is the first step to removing the barrier.

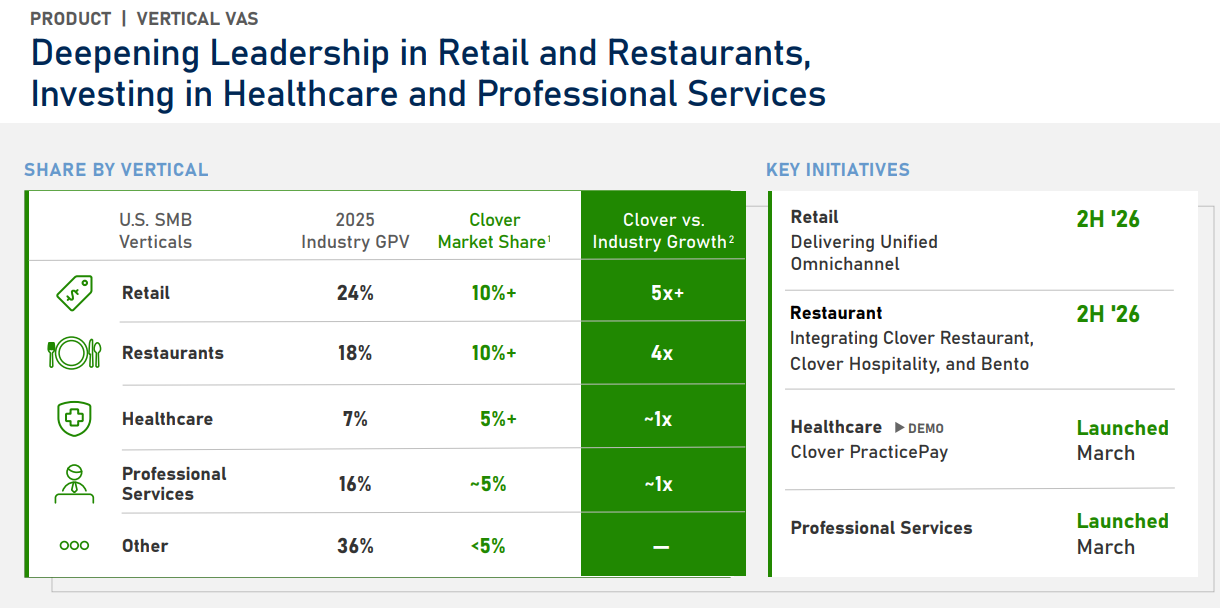

Deepen vertical VAS. Extend Clover’s retail/restaurant playbook into healthcare (PracticePay, launched March 2026) and professional services (also March 2026). Both have ~5% market share today.

Expand horizontal VAS. Clover Capital, Clover Savings, and AI-powered revenue management.

The Goal: Clover revenue growth of 15–20% annually, driving Merchant Solutions to 6–8% adjusted revenue growth through 2029. Key metrics to watch: VAS penetration rate (especially Capital at 4.5% today) and non-Clover conversion volume post-hardware-agnostic launch.

The two issues above highlight what’s broken. What follows is why I think they can deliver it, what success would look like, the key metrics to watch closely, and more.

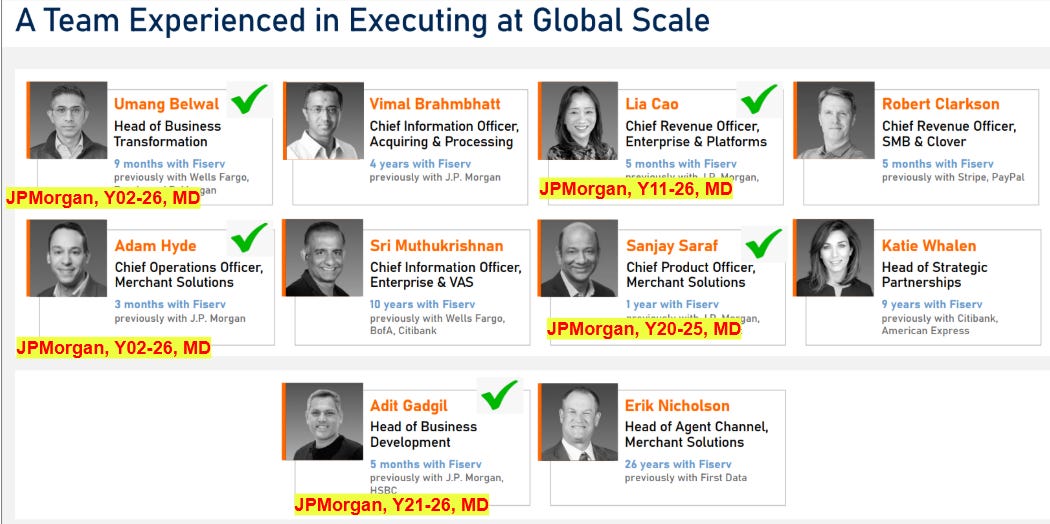

The Executive Team

Lyons appointed two co-presidents and a new CFO, all with long track records and relevant experience. I will highlight one that stands out.

Takis Georgakopoulos (Merchant Solutions): Takis spent 17 years at JPMorgan, leading its payments since 2017. Under his watch, JPMorgan Payments doubled its revenue from $9Bn to $18 Bn (2023) in a highly competitive environment against Stripe, Adyen, and major banks.

The relevance to Fiserv is direct. JPMorgan Payments competes in the omnichannel enterprise space where Carat is. He’s competed against Adyen and Stripe. He also knows bank distribution intimately, which is central to Clover’s go-to-market.

The new merchant COO and Head of Transformation are two 20+year JPMorgan veterans. Takis is recruiting trusted operators into the execution layer. When strong executives bring their own people, it signals genuine conviction, not just a title change.

The broader logic mirrors what I saw at DB and Citi: retain institutional knowledge where it's an asset, recruit outside expertise where the incumbent culture is the problem, and make changes structural rather than cosmetic. Lyons gets this: a JPMorgan payments chief, a Stripe/Optum operator, and a Global Payments CFO. Each business segment retained key executives while adding external braintrusts.

Where the Analogs Hold (or not)

Core banking is the analog that holds. With 40%+ market share, decade-long contracts, and switching costs that make migration unattractive, the franchise is sticky.

FinTech disruptors have under 5% combined share and aren’t gaining. The client losses we’ve seen trace directly to specific, self-inflicted mistakes: poor service quality and forced conversions. The new team has explicitly reversed.

The moat is intact. Management needs time to repair the relationship. That’s precisely the DB and Citi setup: a sound franchise, temporarily mismanaged, with switching costs that afford the new team room to fix it.

The merchant business is the question mark. Clover is competing with Toast and Square, and Carat is competing with Adyen and Stripe. These are real competitors in an environment where switching costs are lower, and the share is contestable. Lyons doesn’t get the same grace period here, and execution must show up in the numbers.

In summary, Core banking gives the turnaround time. The merchant business is where the urgency lives, and where the analog has limits.

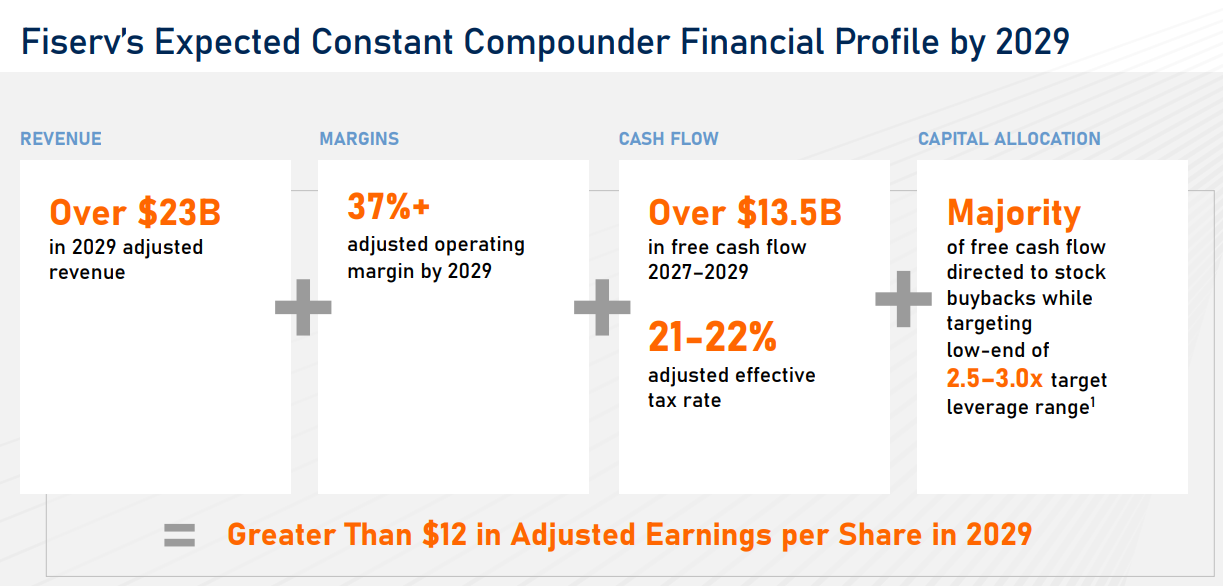

Financial Algorithm

Three levers: moderate revenue growth (4–6% CAGR through 2029), improving margins (37%+), and high free cash flow conversion (90%). Achieve all three, and adjusted EPS reaches $12/share, <5 P/E at today’s price. Committed residual free cash flow goes to buybacks, not empire building.

What I find compelling is the absence of heroic assumptions. None requires anything beyond the competent execution of a fundamentally strong business. If Fiserv simply delivers, the stock looks absurdly cheap in hindsight.

That’s the setup at Deutsche Bank in 2021 and Citigroup in 2022-23. Both set moderate targets. Both would trade at 4–5x forward earnings if targets were met. Fiserv is asking investors to clear the same low bar today.

Closing Thought

Pattern recognition in investing is circumstantial by nature.

But the underlying thesis is the same one that guided me into Deutsche Bank and Citi: a sound franchise, a leader candid about what is broken, a team assembled with credentials and relevance, a modest plan, and a valuation that reflects near-existential fear rather than operational reality. You can find a detailed valuation in the original write-up:

Fiserv’s Investor Day was not a transformation announcement. It was a demonstration of the thinking and discipline I consider essential for a real turnaround.

I have seen this before, and I like what I see here.

I try to recognise similar paterns and I like the idea you have presented. I know it is quite a different company, but many people see Paypal as a turnaround story. Their valuation looks ridiculously low, no debt issues, new management. Have you studied the company? Thanks