Update: Spirit Merger Arb Review before Ruling

Trial, next steps, curve balls, and odds math.

Background

Spirit Airlines SAVE 0.00%↑ currently trades at ~$14.5/share.

Jetblue offered $33.5/share, DoJ filed to block, The trial started on Oct 30, and closing arguments concluded on Dec 5. My initial analysis.

This update covers: “How did the trial go”, “Next steps/curve balls”, “Valuation”, and a few Qs raised in the poll. https://twitter.com/siyul/status/1730981860107309129

Summary Findings (TL;DR)

Jetblue maintains a winning edge, but DoJ has a viable path to prevail. Worth noting that Jetblue’s “Litigating the Fix” is a proven winning strategy in the court in sharp contrast to DoJ’s “only enjoin suffices”. My model raises Jetblue’s winning odds from previously 60% to 70%

I examine 3 curve balls that could cause merger failure even if Jetblue wins the trial, they are DoT’s attempt to block, MAE, and financing failure events. I provide analysis and estimated odds of happening.

I revised odds math based on recent developments, pinned its fair value at $19/share (30% upside to its current price), and analyzed risks and opportunities.

How Did the Trial Go?

You shall watch the YAVB interview with Michael Cohen (report from the courtroom during trial) and the (highly anticipated) upcoming one with Lionel Hutz (attorney specializing in legal SpecSit).

My focus here is to explain why I raise Jetblue's winning odds from 60% to 70% after the trial - primarily due to Jetblue’s “Litigating the Fix” vs DoJ’s “Only Enjoin Suffices” approach. Let me explain:

On a few occasions on Dec 5, during the closing arguments, Judge Young probed a possible path to “Judicial settlement facilitation”:

Judge Young:

"if this isn't enough, but would pass merger with XYZ additional divestitures. What do you think about that?", "Should I analyze that? Should I ask for further hearings on remedy?" (quoted from David Slotinick’s post)

"They want a permanent injunction in what it seems quite clear in this court is a dynamic industry facing unique opportunities & challenges...If I were to fashion an injunction…what sort of limitations or steps for further consideration or review should I build into it?"

Defense responds with a willingness to consider remedies as long as:

“narrowly tailored to specific harm, based on past precedent"

DoJ rejected the remedy route:

Looking at the nature of the harm, it's difficult to envision what kind of remedies could ever offset it. I don't see any kind of remedy other than a full stop injunction.

A full stop injunction is the only thing that would block harm. (from David Slotinick’s post)

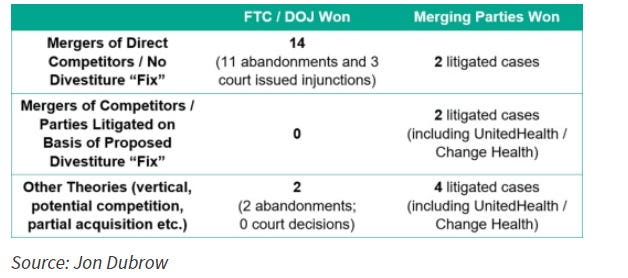

Here is the significance: Jetblue’s “Litigating the Fix”, i.e. the procedure where co. Defending a merger transaction as modified by remedies is a proven winning strategy.

The data (since Biden administration) shows, that when gov (DoJ / FTC) filed an antitrust complaint against mergers w/o Divestiture Fix, Gov won 14 out of 16.

However In 2 cases where merger parties take “Litigating the Fix” approach, Gov lost both cases*.

(*) U.S. v. United Healthcare (Change Health), and U.S. v. Assa Abloy (spectrum brands)

One might argue that 2 cases are not statistically significant, true. But considering the backdrop that 2 sub-scale airlines merge with a divestiture plan in an industry in the top 4 own 80% market share, DoJ isn’t willing to even listen - How would Judge Young address that in his opinion if he rules in DoJ’s favor?

Let us talk about why I think DoJ still has a viable (though narrow) path to win, by legal standards.

As Clayton Action section 7 says:

“the effect of such acqusition may be substantially to lessen competition”

2 things to note:

1). It has been held that the word “may” offers the latitude to not establish the certainty but only a “reasonable probability” of such effect.

2). substantially, has varied interpretations. For example, a classic horizontal merger case, in “U.S. v. Pabst Brewing”, supplying 4.49% of the national beer market met the substantial lessening bar in the court.

DoJ’s viable path to winning relies on 1). its narrow definition of o/d pair as a relevant market, 2). substantially could be interpreted as low as a single-digit market share, 3). merger’s short-term negative impact on certain consumers with a singular focus on unbundled pricing.

Jetblue leans on the “Totality of the circumstances” approach, arguing longer-term (2-3 years, and national market effect), and arguing dynamic attributes that peers can in and out of any o/d pair quickly.

Timeline and Next Steps

Post-trial briefs are due Dec 13.

Judge Young initially signaled to give his ruling by EoY. Considering the two-week trial start date delays, we shall expect the Judge’s ruling by mid to late Jan.

Judge Young’s probing during closing arguments suggests possible complications (thou he repeatedly said not to read much into it) in his ruling (temporary injunction, and additional hearing wrt remedies). If the Judge chooses to go any of these routes, it might add more time and increase the odds of repricing the deal (covered in the valuation section).

It is premature to talk about post-judgment motion, and/or appeal. If there is an appeal, it would be 1st Circuit Court of Appeals, and the appeal needs to be filed within 30 days of judgment.

DoJ’s firm stance on “only enjoin suffices” leaves little room for judicial settlement facilitation. It is still possible but less likely.

Now let us talk about some curve balls if Jetblue wins the trial (Win is defined as a merger that can take place with or without additional remedies).

Curve Ball 1 - DoT Certificate Transfer

In a letter to Sect. DoT (Buttigieg) in July 2022, Senator Warren promoted the idea that DoT has the authority to block airline mergers under Title 49 section 41102 by not approving operating certificates transfer (I post more details on X).

In March 2023, Sect. Buttigieg took a hawkish stance and voiced his support for DoJ’s antitrust case against the Jetblue & Spirit merger.

Note Section 41102 authority to issue/transfer operating certificates has never been used to block a domestic airline merger.

Note that the determination has to be based on “consistent with the public interest”, which the Judge’s ruling would have a similar standard. If DoT chooses that route, it will be in direct conflict with the Judge’s ruling. Imagine what that means if the case goes to the court again.

As the merger is a reverse triangle merger, whether a certificate transfer is required is also debatable.

I think a high probability (>50%) that DoT will voice concerns, and threaten to block the certificate transfer. But its legal case is weak and I model its odds to prevail in court at ~5-10%.

Curve Ball 2 - MAE

Let me start by saying a general MAE clause, followed by well-defined carve-outs (as in this case), is nearly bulletproof. Vice Chancellor Lamb of the Delaware Chancery Court issued the opinion in Hexion v. Huntsman Corp, GFC, rejecting Hexion’s MAC claim in Sep 2008.

it was not a coincidence that “Delaware courts have never found a material adverse effect to have occurred in the context of a merger agreement.”

the occurrence of a MAC must show that “there has been an adverse change in the target’s business that is consequential to the company’s long-term earnings power over a commercially reasonable period, which one would expect to be measured in years rather than months.”

IMO, Spirit aircraft grounding due to RTX Engine issue is not even an arguable MAC event and stands no chance. Barring extraordinary future events, I model MAE 0% odds to effect merger failure.

Curve Ball 3 - Financing

Jetblue has committed debt financing, and the closing is not contingent upon it. i.e. Jetblue must use reasonable best efforts to obtain alternative financing in the event of financing failure event.

The commitment letter is subject to confidential requirements, thus we don’t know the term details. However, it is reasonable to assume it is seller-friendly, and consistent with the merger agreement, including similar MAC language.

The only possible scenario I can think of to trigger a debt financing failure event is via solvency: likely comparable to the solvency defined in section 4.8 - the combined company on a consolidated basis, including balance sheet test, ability to pay debts, and not left with unreasonably small capital.

Diving deep into both entities’ balance sheets and contractual obligations is beyond the scope here. My quick take is it shall pass all tests, but as both companies currently operate under various macro headwinds, arguments could be made it might fail the solvency test at the time of closing.

However, if a financing failure event takes place, Jetblue still needs to make the Best Available Efforts to secure alternative funding, with its combined unencumbered assets (>$5Bn). Certainly that adds a lot of unknowns but I consider the odds of financing effect merger failure reasonably low, ~10%.

Valuation / Positioning

Here valuation is odds-based math, with little to do with the fundamentals.

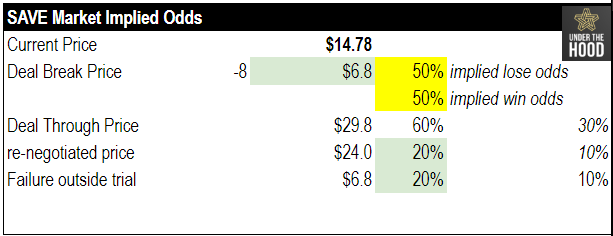

My model suggests Spirit's fair value at $19/share (currently $14.5/share).

My model assumes Jetblue win odds to 70%, Spirit deal-break price $7.

If Jetblue wins, a 60% chance sticks to the original deal, 20% odds repricing, and 20% odds failure (due to DoT and/or solvency).

Another thing I watch is the implied odds gap between EQ and Options. At the current price of $14.8/share, the implied odds for Jetblue winning the trial is 50%.

I also monitor Jan to Mar call options (strike price $15 to $20).

The implied odds are determined largely by the same variables as equity (excluding deal-break price), plus the probability that the ruling is certain by expiration dates.

To get implied odds, I take a trial-and-error approach to adjust modeled trial win odds (#3) and Jan, Feb, and March certainty odds (#4) to narrow the gap between the Modeled Odds Price and Current Option price (#5).

This is not perfect, with many minor adjustments, and common-sense judgment, and my current option implied odds of Jetblue winning is 53%.

My key takeaways are:

EQ and OPT odds gap is about 3% (EQ = 50%, OPT = 53%), that gap was near 0 when I wrote my initial work in Oct and expanded to the max around 20% (in late Nov).

A lower strike price call (e.g. $15) option seems to demand a premium compared to higher price ones (e.g. $20 call). Caution not to draw a quick conclusion that $20 call is a better buy as it could be caused by other factors, e.g. market perceived recut price is lower than my model, etc.

I built my initial position in early Nov mostly in $15 to $20 (Jan-Mar) call options and gradually added the equity as I observed the increased premium in Options (peaked in late Nov).

Partially due to the reasons discussed in the article, I’m increasingly less comfortable with Jan's call options - I still hold some but the majority of my position is in equity now. I try to avoid being right in direction, but wrong in timing.

Parting Thoughts

If you are still with me, thank you and I appreciate it.

My work is tailored towards curious-minded investors, who like to explore new ideas/industries, dig deeper, and make their own decisions. My goal is to be a part of your research process, provide relevant info, and offer your insights/model to project what the future holds.

If that is of interest to you, please subscribe and share it with your friends.

Reference

MAC Clause: here

Clayton Action Section 7 review: here

Assessing the state of affairs in FTC/DoJ merger enforcement: here

On the DoT transfer, the post-merger structure doesn’t require certificate transfer to my knowledge (I may have missed something). I understand the ultimate plan is to consolidate the entities, but that becomes a timing issue in 18-24 months rather than impacting the merger.

Is your understanding different? If not, why factor this DoT block risk into probabilities?

Cheers

A/C

Thanks for the update, Siyu, great work, as always.

I am long SAVE but one sticking point I have, at least in theory, is what would a "reasonable" remedy be? There doesn't seem to be an obvious answer in the same way there was with a case like SPB/ATVI etc. I agree that we could think of many, perhaps countless, technical remedies that would nullify DOJ concerns but in the same way that I believe Judge Young doesn't want to issue the permanent injunction the DOJ requests because of its dogmatic nature, I think he would also be hesitant to create a 'regulated' market by crafting a solution that required 'x' seats on 'offending' routes on JBLU planes to be unbundled/basic etc not because that wouldn't work, but because who would do the monitoring? What would the reporting mechanism be? While I obviously think the DOJ is being over the top with their dogmatic views, I do have some empathy that there doesn't appear to be a particularly 'clean' solution. Would you disagree? Do you see a relative clean solution that Judge Young could actually get on board with if it were presented to him?