When a Helmet-Wearing CEO is Needed

failed pivot, weak bs, neglected quality assets, scream for a right leader.

The Setup

Today’s story concerns a mining company with quality assets that lost focus as its former CEO pursued distraction (and failed) amidst a challenging macro environment.

Following many equity raises and losing 90%+ in stock value, an experienced operator stepped in as an advisor before becoming CEO. He brought along his team, wrote a big check, and initiated turnaround efforts.

It is Americas Gold and Silver Corp USAS 0.00%↑, a small-cap silver mining company

Thesis Highlights

USAS is a turnaround bet. Mining turnarounds often share common elements: good mining assets facing setbacks, but can be resolved with an effective team and a favorable macro setup.

USAS has it all.

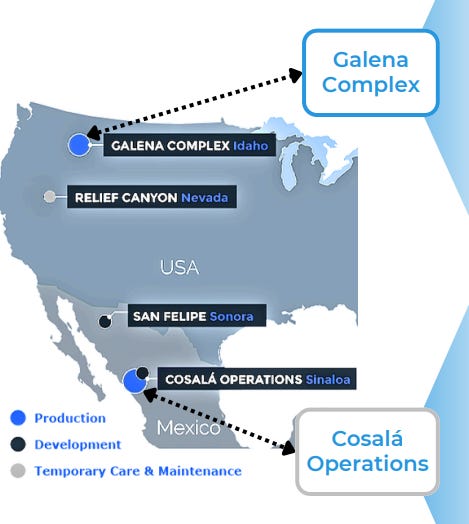

Good Assets: USAS’ Galena Complex is located in the most prolific silver-producing district in the US (and top 3 worldwide), produced 230Moz silver from 1953 to 2015 (avg 3.7Moz a year), with a solid track record and established infrastructure.

Setbacks: The former CEO’s pivot to gold (2018) with undisciplined acquisition and exploration led to an exhausted balance sheet and neglected crown jewel silver mines, desperate for revival.

Right Team: Eric Sprott (largest USAS shareholder) and Paul Huet (CEO/Chairman, own 3.6% USAS) combined operational know-how, industry connections/funding, skin in the game, and a proven track record of junior mining turnaround (Karora Resources in 2018-2024). Turnaround efforts are under way, picturing a hands-on boss wearing a helmet onsite. Ample evidence suggests it will work, as I discuss in my research.

Favorable Macro Setup: Silver has finally turned a corner after a decade of challenges in the market, recently exceeding its 10-year high.

Outline

I will first brief the backdrop: Silver’s history, unique dual-role, increasingly wider demand and supply gap, and why it presents a compelling setup.

I then cover company-specific aspects to explain why I believe this is a credible turnaround story. I reveal the actual quality of its mining assets, analyze its previous failures, and assess the current turnaround strategy, emphasizing the key personnel involved.

I will end with napkin math, valuation model, and my positioning strategy.

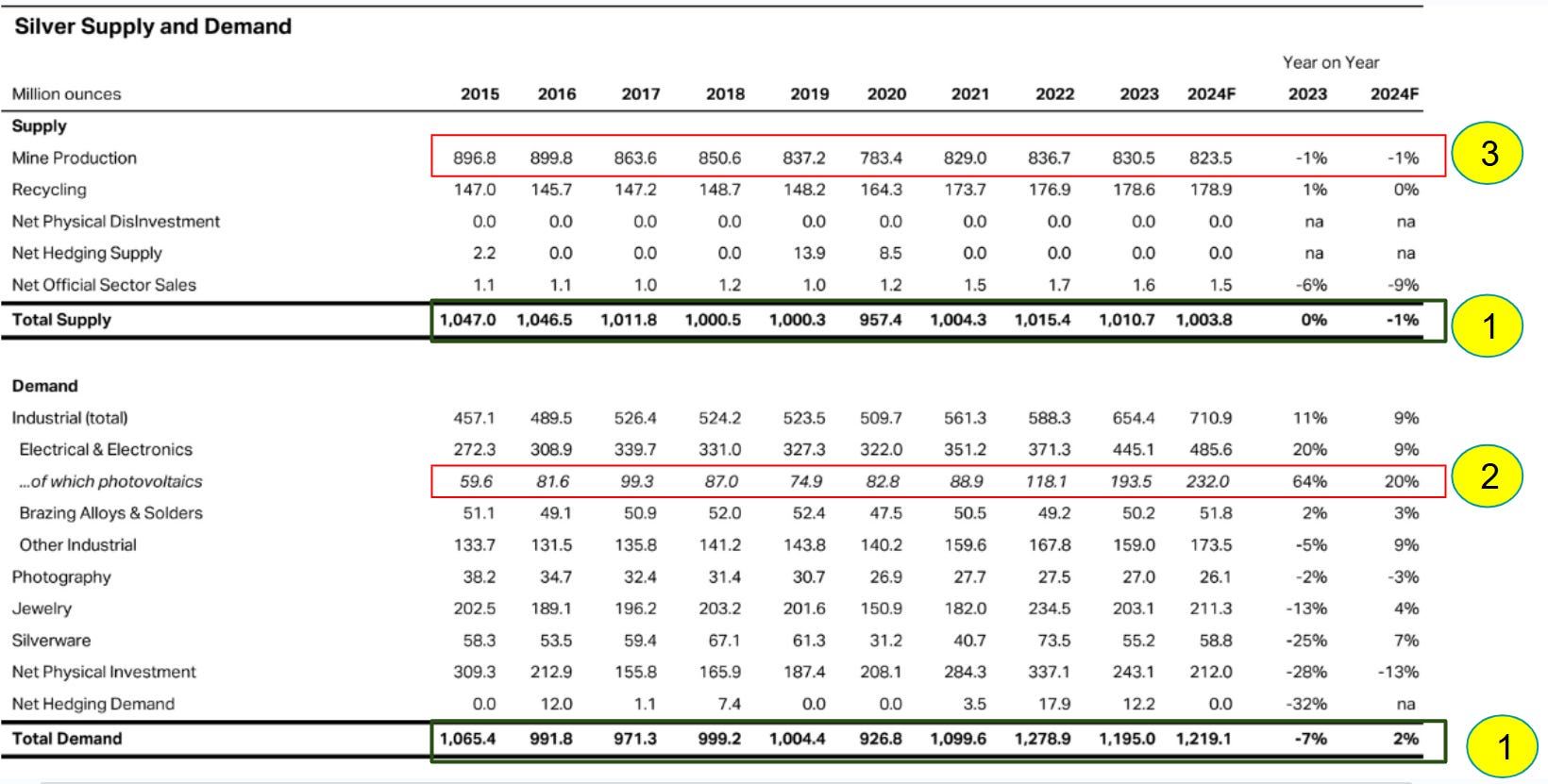

Silver

has a rare dual role as both a commodity and a store of value. World Silver Survey 2024 (below) shows Silver’s Supply and demand dynamics since 2015:

Supply remains flat (~1000Moz/y), and demand has steadily increased since 2020. Strong industrial needs drive the increased supply-demand gap.

60% of the demand originates from Industrial needs. The recent year demand increase mostly comes from Solar Panel needs (Y15’s 60Moz to Y24’s 230Moz). Other major categories, e.g., jewel/investment, largely remain flat.

Despite the volatile Ag price (high ~$50/Oz in 2011, low $15-$20/oz between 2014 to 2019, recently over $30/Oz), Silver mining output remains flat.

Why has Silver mining output remained flat despite volatility? It is multi-factored. One contributing factor is that 70-80% of silver mining is a by-product of other metals (mostly copper, zinc, lead, and Gold). Polymetallic mines only switch their primary metals after dramatic and sustained price changes that fundamentally alter unit economics (volatility alone won’t trigger this), as it requires significant capital investment and a long time horizon to implement the change. We will address that subject later.

Silver demands are grouped into three categories.

Jewelry/silverware (~20%+ in Y23): stable at 200-250Moz a year

Investment (~20% in Y23): Coin, bar, and ETF

Industrial (55%+ in Y23): slightly under half from Solar panels, offsetting the photography decline (peaked at 270Moz in Y99).

Solar panels are the primary driving force behind Silver’s increasing demand. It was from 2-3Moz in 2000 to 230Moz in Y24 (20% total demand), projected to rise to 25% demands in Y25. If Solar reaches 1000GW/year by 2030, modelling 0.04g/W of silver usage, it will require 300-400Moz.

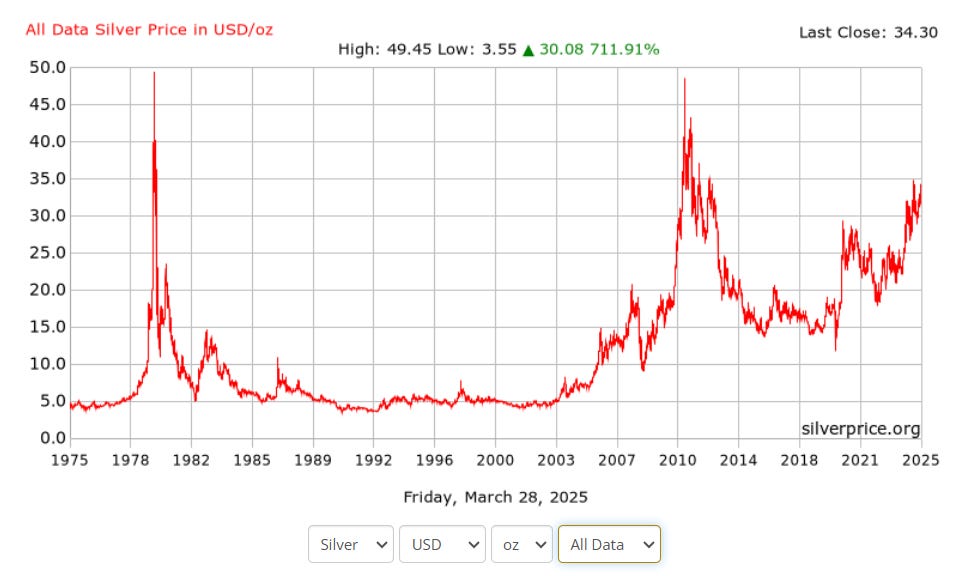

Past Cycle: This chart adds some color to “silver is a volatile commodity”: with inflation, a weak dollar, and geopolitical instability, Silver rose from $5 to ~$50 and back to $5 in less than 5 years (1978 to 1982, peaked in 1980)

USAS History: M&A

Started as Scorpio Mining, a single silver mine in Mexico in 1998, through multiple M&A*, Americas Gold & Silver (USAS) grew to have two operating mines (Cosala in Mexico and Galena in Idaho), one in development, and one (Relief Canyon) in maintenance today.

Past M&A*

Y2010: Acquired Platte River Gold (San Rafael, and El Cajon)

Y2014: Merged with U.S. Silver (Galena Complex)

Y2018: Acquired Pershing Gold (Relief Canyon), rebranded as Americas Gold & Silver

Its 2018 Pershing Gold acqusition and pivot to Gold marked a turning point, leading to over $ 160M in spending (~$ 40M acquisition, $ 100M construction CapEx, and $20M+ OpEx). It led to a failed project with no economic output.

USAS History: Dilutions

The history of USAS is a poignant tale of ongoing equity dilution.

Its total shares grew from 39Mn in 2017 NYSEAm dual-listing to 275Mn in Sep 2024 before the recapitalization, mainly to facilitate the Pershing Gold acquisition and subsequent equity raise to fund its operation and finance its failed Relief Cannon project.

2017: dual-listed in NYSE American, 39Mn shares.

2019: acquired Pershing Gold, shares increased to 77.3Mn.

2020-2022: Increased to 200Mn shares by EoY2022, multiple bought deal financing and ATM offering, at $1-3/share range.

Sep 2024: 275Mn before Recapitalization.

USAS History: 2024 Recapitalization

By mid-2024, USAS had a failed Gold mine and two poorly maintained Silver mines that burn cash and use equity financing as the lifeline.

2024 recapitalization issued a total of 305Mn shares, 117Mn shares to Sprott to exchange for his 40% interest in Galena Complex, 53Mn to management, including Paul Huet’s 23Mn shares, and 125Mn share Private Placement. Management and Private placement shares were priced at ~$0.3/share.

The sequence of events that led to this point was ugly: a team with no focus, burning-cash mines, and equity dilution as a lifeline. Before discussing the turnaround story, let's introduce Eric Sprott and Paul Huet and explain how they got involved in this setup.

Sprott & Huet

For those unfamiliar with the precious metals sector, Eric Sprott is to precious metals what John Malone is to cables, with a focus on junior mine investing.

Eric made his initial $10Mn (4Mn shares) equity investment in USAS in 2019 (8% outstanding then, diluted to ~0.7%) and committed a $20Mn to revive Galena (in exchange for 40% Galena interest). He subsequently participated in more funding rounds, investing ~$40Mn.

In late 2023, he brought in his trusted partner Paul Huet (a mining operator) as a technical advisor to assess “what the hell is going on?”. In Sep/Oct 2024, the company nominated Paul as USAS CEO/Chairman, and Paul orchestrated a 3-way recapitalization.

Eric and Paul’s relationship back to Karora Resources (KRR), while Eric was the cornerstone investor and Huet joined in 2019 as Chairman/CEO, turned a financially struggling, money-losing mining micro-cap into a high-quality gold producer and was acquired by Westgold at C$1.2Bn in July 2024.

Double-click Past Events

Eric invested $40Mn in Galena and USAS and was reportedly unwilling to convert its 40% Galena ownership to USAS equity as he lost confidence in the team.

Paul was CEO of Karora when initially appointed as a USAS advisor. Paul started engaging in USAS investment proposals in Feb 2024. After Karora’s merger with Westgold, he and his team had multiple job offers but chose to join USAS and participated in an equity raise. (Paul became a 3.6% owner, reportedly the single largest investment he ever made. His team & BoD collectively bought ~5% equity)

Both Eric's and Paul’s actions are bullish.

What did Paul see?

He saw a high-quality asset (Galena) hindered by years of negligence and issues, but mostly solvable with an experienced and focused team through operational hardening and adequate capital improvement. Assets, Team, and Capital - He brought all 3 key elements together with the 2024 recapitalization.

Keep reading with a 7-day free trial

Subscribe to Under The Hood to keep reading this post and get 7 days of free access to the full post archives.