TripAdvisor: A Perceived Value Trap with Asymmetric Risk Reward

Obstacles being resolved, valued at 5x Ev/ebitda, near 10Y low.

Intro

The company features one of the most extensive user review platforms for travel (hotels, restaurants, tours, etc.), and it has the largest (and rapidly growing) platform for booking travel experiences.

Facing two persistent detriments (competition from Google and a concerning dual-class structure), its stock performance lags behind peers for years.

Recent developments are reshaping both: Dual-class is poised to be resolved, and Google's pressure is gradually becoming less critical. Yet, the stock is near its 10-year low.

That enters Tripadvisor TRIP 0.00%↑

Some readers might be inclined to reject the idea immediately, thinking TA’s core is a sunset business. I largely agree with that notion, and you will find even my most bullish case models a 5% annual decline in perpetuity. Yet my model shows a compelling opportunity.

Thesis Highlights

Resolved Dual-class Detriment: When Tripadvisor acquires Liberty Tripadvisor (expect to close in 2Q25), it eliminates the dual-class structure and unlinks a financially unstable parent company. Tripadvisor will finance the transaction with its balance sheet, incurring no additional debts.

Marginalized Google Detriment: TA’s dependence on Google continues to reduce as its core business becomes an increasingly smaller portion of its revenue (from 75% in Y19 to 49% in Y24) pie.

It is cheap, valued at 5.1x Ev/Ebitda. Its $1.8Bn EV has a ~10% downside under my Bear model and a 60% to 130% upside under Base/Bull models as we examine its two key segments:

Tripadvisor Core: despite facing Google’s competition (some would call it unfair), it is still a cash-generating machine. It can generate nearly $700Mn FCF in the next 6 years, even in a punishingly bearish scenario.

Viator: it alone can be worth the entire EV today, even using the lowest Price/Sales valuation among its peers.

In this research, I will explore recent events poised to resolve and marginalize two persistent detriments. I will also discuss TA Core and Viator business and its valuation.

Resolving Dual-Class Structure

Greg Maffei, Liberty Media’s recently stepped-down CEO, is Tripadvisor’s largest shareholder through Liberty Tripadvisor (LTRPA/B). Liberty Tripadvisor is a holding company with 21% equity interest and ~57% voting rights via a complex structure (tracking stocks and supervoting dual-class). Greg Maffei holds all supervoting rights.

Liberty Tripadvis took out ~$400 margin loans in 2014 and paid $350Mn as a dividend to its parent company, Liberty Interactive, before the spin-off. The debts were refinanced and changed hands over the years, with an increasingly higher loan-to-equity ratio as Tripadvisor’s share price declined.

There are many rabbit holes to explore1, but the key is that Liberty Tripadvisor’s common equity has a negative value when it drops below $17.

Tripadvisor dropped below $17 in August 2024. Meanwhile, Liberty Tripadvisor’s $330Mn debts and Series A preferred are due / have mandatory redemption in March 2025; that combination rang an alarm bell.

It is similar to Paramount Global when National Amusements had overwhelming debt obligations, and Sharon Redstone was forced to sell. The final “solution” favored supervoting rights owners at the expense of the commons.

Surprisingly, on December 19, 2024, Tripadvisor announced a common shareholder-friendly merger plan with Liberty Tripadvisor. The plan pays ~$0.26 for each LTRPA/B share (a total of $20Mn), repays $330Mn in debts, and pays $42.5Mn in cash + 3.04Mn Tripadvisor shares for preferred series A.

In summary, at a total cost of $435Mn ($392Mn cash + 3Mn shares), it retires ~27Mn shares (including all supervoting B shares), eliminating the dual-class structure.

Liberty Tripadvisor equity shareholders will receive a symbolic payout, and no premium is assigned to the supervoting B share. This is a massive positive for TRIP Commons, and the Market (only) welcomed it with a 7-8% rise the next day, way too moderate in my view.

Less-weighted Google Factor

Tripadvisor core has one critical weakness: 75% of its traffic comes from organic search, specifically Google. Google’s integration of user reviews into Search and Maps and its ever-changing search algorithm have a material impact on Tripadvisor’s website and app traffic, putting constant pressure on TA’s business model, revenue, and profitability.

Barring a meaningful remedy ruling against Google (the next trial date is April 22, 2025), TA’s core business will permanently decline with a dim long-term prospect.

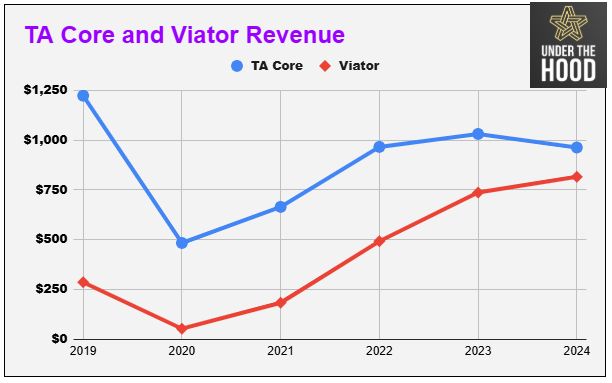

In the meantime, TA core is quite a profitable business and requires small CapEx. Equally important, since Matt Goldberg became CEO in July 2022, TA has made critical strategic moves. However, as a percentage of total revenue, its core business declined significantly from 75% in Y19 to 49% in Y24 (LTM). The chart shows that TA core recovered 75% of its Y19 level, while Viator business has grown 3x since 2019.

Viator has become an increasingly important part of Tripadvsior’s valuation story.

Viator

Viator was founded in 1995 and acquired by Tripadvisor in 2014 for $200Mn. After a sharp decline in 2020 and a moderate bounce in 2021, Viator experienced two years of triple digital revenue growth in Y22 and Y23. While growth slowed, its high operating leverage and improved take rate have turned the business profitable since 3Q23.

In its recent 3Q24, it had $1.1Bn GBV (Gross Booking Value), a 24% take rate, and $270Mn revenue. It also achieved $30Mn EBITDA (11% EBITDA margin, up 400 bps year over year), the highest quarter ever.

As the most prominent online travel experience booking platform globally, it has an unparalleled advantage (in addition to its scale) as TripAdvisor acts as its top funnel.

As Viator grows, it is also mindful of ensuring profitable growth. More importantly, it applies lessons from Tripadvisor, focuses on direct search, and minimizes dependence on Google. Some recent management commentaries:

3Q24 on growth/profitability balance and paid vs direct market channel

In the Viator segment, we've been balancing growth and investment to drive scale and contribute an increasingly larger share of revenue and profit to the group.

While we continue to see healthy growth in our paid marketing channels, our direct channels beyond search are growing faster

2Q24 on Viator profitability from lower marketing costs

Importantly, our repeat users come with lower marketing costs. Viator adjusted EBITDA was %10 million or 4% of revenue in the quarter. The year-over-year margin leverage of approximately 500 basis points was driven primarily by lower sales and marketing as a percent of revenue as a result of a more favorable free versus paid channel mix.

It is also actively reducing dependence on its 2 largest distributors, Expedia and Booking.com, from 47% in Y13 to 35% in Y22 and 25% in Y23.

Midway Recap

Tripadvisor is a tale of two cities. Its core business is gradually declining, while Viator is a dominant experience booking platform that has recently become profitable and has high operating leverage.

It has a few other brands, most prominently theFork, a restaurant booking service, but they’re relatively immaterial to Tripadvisor’s valuation story.

In the sections below, I use Discount Cash Flow (DCF) to model TA core business; I will compare Viator to its peers, both public and private M&A transactions.

Valuation

The presented models assume the “Transaction” (Tripadvisor’s acquisition of Liberty Tripadvisor) will go through as announced in December 2024. Tripadvisor has 126.5 million A and 12.8 million B shares today; the Transaction will buy back all B and 16.4 million A shares and issue 3 million shares to the preferred shareholders, thus leaving a total of 113 million outstanding shares.

TA has $1.1Bn cash and $0.8Bn debts as of 3Q24. It will spend ~$0.4Bn on the acqusition, thus $0.1Bn net debt after the Transaction.

113Mn shares, $15/share, $1.7Bn market cap, adding $0.1Bn net debt to $1.8Bn Enterprise Value. With $350Mn LTM Ebitda, it is valued at 5.1x Ev/Ebitda.

Quite intriguing at first glance, let us dive into each segment.

Valuation - Core

TA’s core business generates $350Mn Ebitda LTM (32-34% Ebitda margin). I model 10% ($30Mn) CapEx and 20% (60Mn) Tax, which comes to 70% Ebitda to FCF conversion.

Note: Tripadvisor’s total CapEx has been between $55Mn to $65Mn for the last 3 years; I model an even split with Viator to get to $30Mn CapEx for the core. Also, its interest expense and interest income roughly match.

The table below is my Base scenario. It models a 10% revenue decline annually and a 200bps EBITDA margin decline a year till it hits 20% (then lower to 15% after 12Y), using an 8% discount rate and a 70% EBITDA to Cash flow conversion rate.

It gets to $0.85Bn NPV using 15 years of DCF. The table shows NPV with accumulated FCF for each year, and you will notice its 10Y, 15Y, and 20Y NPV are very close (between $0.81Bn and $0.87Bn), as rapid revenue decline (10% in this case) model makes future years cash flow’ cash flow neglectable.

Keep reading with a 7-day free trial

Subscribe to Under The Hood to keep reading this post and get 7 days of free access to the full post archives.